Mortgage demand fell by 4.5% in the March quarter of 2024 compared to the previous year, yet challenges persist as both the average limits and arrears on these loans continue to increase, according to Equifax.

“Over the past year, refinancing has been a key driver of mortgage demand as consumers who were reaching the end of their fixed-rate period sought out better deals,” said Kevin James (pictured above), general manager advisory and solutions at Equifax. “Many of these mortgage holders have now refinanced and this demand has dropped off.”

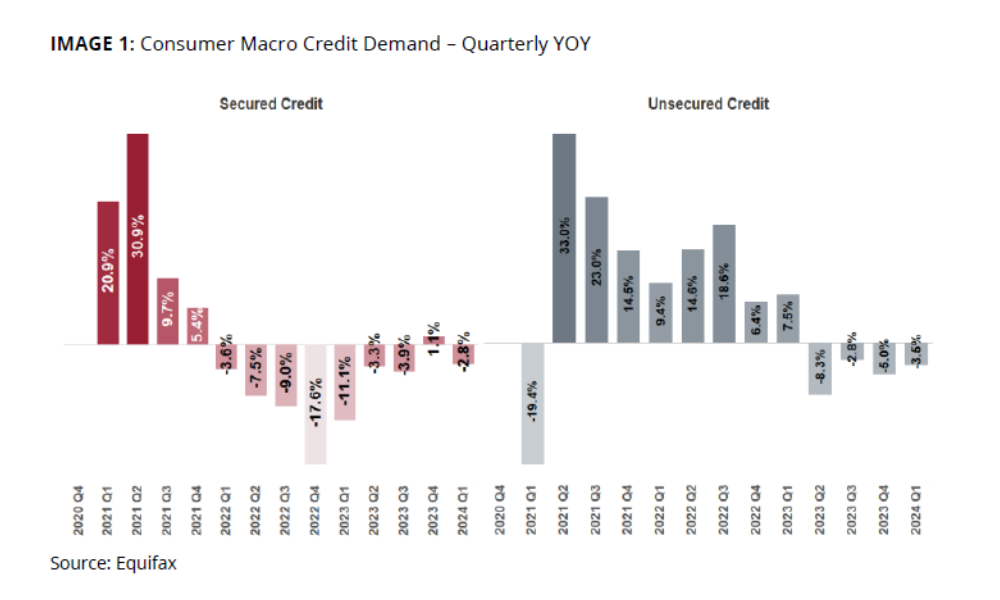

The latest Equifax Quarterly Consumer Credit Insights showed that in Q1 2024, secured credit demand, primarily from mortgages and auto loans, decreased by 2.8% compared to the same period in 2023.

The Equifax report, which measures the volume of credit applications for credit cards, personal loans, buy now pay later (BNPL), mortgages, and auto loans, also found that despite stable interest rates, mortgage stress is intensifying.

“While mortgage demand has declined, the average limit per new mortgage account continued to grow at a consistent pace of 7% year-on-year – reflecting increasing house prices,” James said.

“Additionally, we’ve seen higher mortgage stress this quarter despite stable interest rates; mortgage arrears increased across all categories. Arrears of 30-89 days past due increased 15% year-on-year, while arrears of 90+ days past due were up 17%.”

While overall unsecured credit demand saw a decline of 3.5%, demand for credit cards surged by 13.2% compared to the same period last year. The increase contrasts sharply with the declines seen in personal loans (-4.6%) and BNPL services (-24.7%).

“We’ve seen a significant uplift in credit card demand, with many Australians reaching out for unsecured credit to alleviate cost of living pressures,” James said. “We’re also seeing strong growth in credit card limits, up 29% year-on-year, which means consumers are applying for more money on their cards.”

The financial strain on consumers is evident not only in the demand for higher credit card limits but also in the growing arrears across various credit types. Personal loan arrears have reached their highest point since 2020 and are expected to peak in the second quarter as holiday expenditures become due.

“While demand for personal loans has dropped, arrears in this portfolio are rising,” James said. “In fact, personal loan arrears of more than 30 days past due have hit their highest point since 2020. And we expect this trend to continue – personal loan arrears tend to peak in Q2, as festive season spending becomes due.”

To compare the latest figures with the previous results, click here.

Get the hottest and freshest mortgage news delivered right into your inbox. Subscribe now to our FREE daily newsletter.