You've probably heard about the gender pay gap and the superannuation gap, but there's another critical gap that often goes unnoticed: the gender property gap.

CoreLogic's latest Women and Property report sheds light on this overlooked issue, revealing some striking revelations.

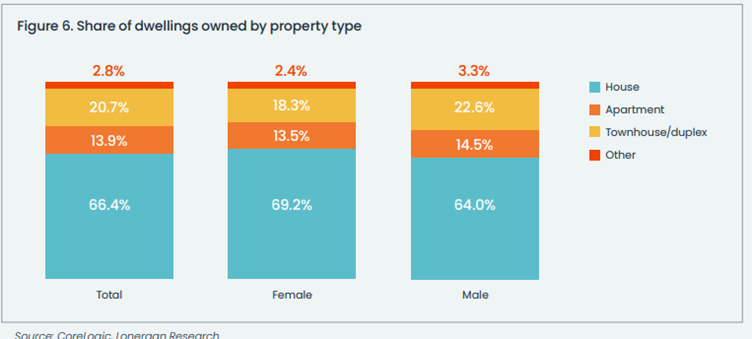

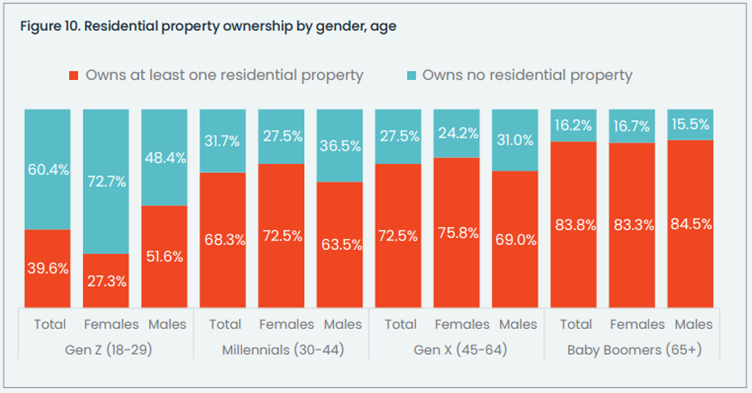

Initially, it may seem like progress when considering overall property ownership rates: women slightly surpass men, with a 68.7% ownership rate compared to men's 67.4%. However, a closer look reveals a different story, especially among younger generations.

The survey exposes a stark contrast among Gen Z individuals, where only 27.3% of women under 30 own residential property, in contrast to 51.6% of men. This 24.3% gender property gap underscores the urgency for action.

Mortgage broker Alex Veljancevski (pictured above) emphasised the importance of understanding these trends, particularly when serving young female clients.

“All brokers, regardless of gender, should examine this gap and consider how to adjust our services to better meet our clients' needs and narrow the divide,” Veljancevski said.

Delving deeper, CoreLogic's research highlights disparities in investment patterns. Males maintain a higher rate of investment in residential dwellings, with 14.1% owning at least one residential investment property compared to 12.5% of females.

The survey also asked about other forms of property investment, providing the examples of commercial property, industrial property, or vacant land. Just 2.2% of males reported having at least one other form of investment property, slightly higher than 1.2% of females.

Moreover, the report touches on the valuation and debt dynamics, revealing intriguing insights.

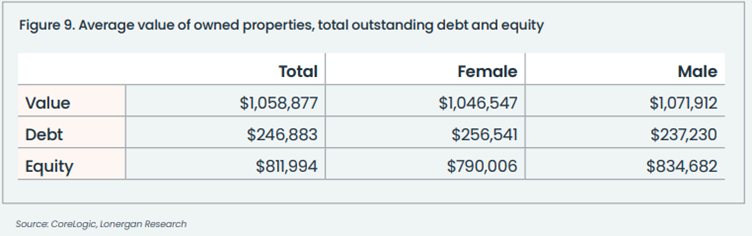

Despite women owning a higher proportion of houses, typically more valuable than units, their average reported value is slightly lower than that of men ($1,046,547 for women compared to $1,071,912 for men).

Female-owned property values tend to cluster between $500,000 and $1,499,999, while men's properties show a flatter distribution.

Despite this, women report slightly higher average outstanding debt, resulting in a lower overall home equity position.

The way women buy property also contributes to the gender property gap.

Joint ownership emerges as a prevalent avenue for women to access the property market, with more women than men using this arrangement.

For women on lower income, this can be an effective way to get onto the property ladder sooner through sharing of housing costs. However, this has its own complexities potentially creating situations of financial dependence and financial abuse.

This may also pose some vulnerability for women who are single, or those that experience a relationship breakdown.

Affordability constraints significantly contribute to the gender property gap, particularly among younger generations. While women may aspire to homeownership, limited financial resources often pose a significant barrier.

Respondents earning less than $100,000 annually exhibit a home ownership rate of 61.4%, compared to 86.6% among those earning more than $100,000.

Various factors contribute to this gap. Age plays a crucial role, as both home ownership and higher incomes are typically achieved later in life. Additionally, socio-economic background influences access to property ownership, with higher-income individuals often benefiting from family wealth or inheritance.

Interestingly, women maintain a higher rate of property ownership when income is considered. For women earning less than $100,000, the ownership rate was 62.1% (compared to 60.6% for men), rising to 91.0% for those earning over $100,000 (83.2% for men).

However, the notable gap that persists among Gen Z respondents (51.6% of men own a property compared to only 27.3% of women) can partly be chalked down to differences in income.

Gen Z women, on average, have lower incomes and are much more likely to engage in part-time or casual employment.

This finding is intriguing because discussions about earnings for men and women often centre on the well-documented gap resulting from older women assuming unpaid parental or caregiver responsibilities.

“Clearly, affordability constraints exacerbate the gender property gap among young people, underscoring the need for targeted interventions to address this systemic issue,” Veljancevski said.

While affordability constraints play a role, they do not fully explain the gap's persistence. Veljancevski identifies three main factors.

First, the average man earns more than the average woman – for every $1 earned by men, 88c is earned by women, according to the Workplace Gender Equality Agency.

Second, “men are more financially risk tolerant than women”, according to a paper in the Journal of Economic Behavior & Organization.

Third, men have higher levels of financial literacy than women. In the Household, Income and Labour Dynamics in Australia survey, which asked respondents five questions on financial literacy, the average scores were 4.0 for males and 3.5 for females.

Addressing these disparities requires a multifaceted approach.

Part of the reason the gender pay gap exists is because men are more likely to be in positions of authority than women.

“Because humans are more likely to favour (often unconsciously) people like them, it means, all things being equal, that men are more likely to hire and promote men than women,” Veljancevski said. “That would apply as much to the mortgage broking industry as society in general.

“So if the industry made a conscious effort to increase the share of female representation – only 26.9% of brokers are women, according to the MFAA – we’d be able to narrow the pay gap, at least in our industry.”

“Brokers – especially male brokers – need to recognise that the average woman requires more reassurance around buying property and taking on debt than the average man,” said Veljancevski.

“That means we have to provide the average female client with more education.”

“We also need to recognise that the average woman has less financial literacy than the average man. Again, that calls for more education – but it has to be delivered in a way that feels empathetic rather than patronising.”

Ultimately, closing the gender property gap is not just a matter of equality; it's about empowering individuals to achieve financial security and well-being.

Brokers, as key players in the financial landscape, have a pivotal role in driving this change.

How do you service your young female clients? Comment below.